The fundamental concept of profit and loss is used in every company and business. Profit and loss are not only useful to run a business or company but also to keep a track of your own expenditure. Discount which is also a part of this concept in a way is something that helps compare prices. It is also a form of profit and loss by which we can learn to save money by buying the same article at a comparatively cheaper price.

‘Profit and Loss’ is thus a concept developed from various applications to real-life problems which take place in our lives almost every day. When a good is re-purchased at a greater price then a profit is incurred. Similarly, if the good is repurchased at a lesser price then there is a loss.

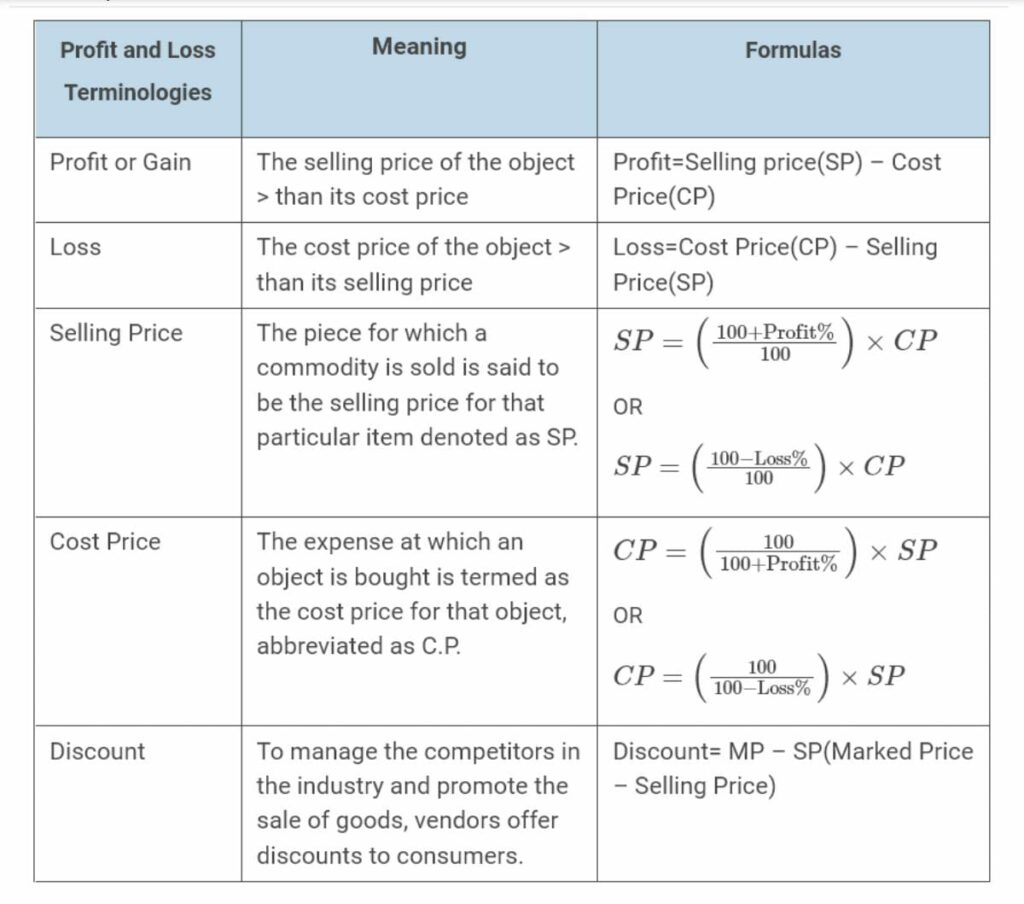

Terms related to Profit and Loss

Cost Price (CP)

The price at which an article is purchased. Sometimes it also includes overhead expenses, transportation costs, etc. For example, you purchased a Television Set at Rs 20,000 and spent Rs 5000 for transportation and Rs 1000 for setting up. So the total cost price is the sum of all the expenditure, that is, Rs 26,000.

TYPES OF COSTS

1. Direct or Variable Costs – This is the cost associated with the direct selling of a product/service. In other words, this is the cost that varies with every unit of the product sold. Hence, if the variable cost of selling a pen for 20 is 5, then the variable cost for selling 10 units of the same pen is 10×5=50.

2. Indirect Costs or Fixed Costs – Some types of costs have to be incurred irrespective of the number of items sold and are called fixed or indirect costs. For example, irrespective of the number of units of a product sold, the rent of the corporate office is fixed. Now, whether the company sells 10 units or 100 units, this rent is fixed and is hence a fixed cost.

3. Semi Variable Costs – Some costs are such that they behave as fixed costs under normal circumstances but have to be increased when a certain level of sales figure is reached. For instance, if the sales increase to such an extent that the company needs to take up additional office space to accommodate the increase in work due to the increase in sales then the rent for the office space becomes a part of the semi-variable cost.

Selling Price (SP)

The price at which an article is sold. It may be more than, equal to, or less than the cost price of the article. For example, if a vendor bought an umbrella at Rs 400 and sold it at Rs 500, then the cost price of the chair is Rs 400 and the selling price of the umbrella is Rs 500.

Profit (P)

If an article is sold at a price more than its cost price then we make a profit. For example, the land was purchased at Rs 1lakh and two years later it was sold at Rs 3lakhs, Profit made is 2lakh.

PROFIT = SELLING PRICE – COST PRICE

Loss (L)

If an article is sold at a price less than its cost price then a loss is incurred. For example, a car is bought at Rs 5lakhs and a year later it was sold for Rs 2lakhs then the seller incurred a loss of Rs 3lakhs.

LOSS = COST PRICE – SELLING PRICE

Marked Price (M.P.)

It is the price that is marked on an article or commodity. It is also known as list price or tag price. If there is no discount on the market price, then the selling price is equal to the market price.

Markup: It is the amount by which cost price is increased to reach market price.

Markup = MARKED PRICE – COST PRICE

Profit Percent (P%): It is the percentage of profit on the cost price.

Loss Percent (L%): It is the percentage of loss on the cost price.

BREAK-EVEN POINT

The break-even point is defined as the volume of sales at which there is no profit or no loss. In other words, the sales value in terms of the number of units sold at which the company breaks even is called the break-even point. This point is also called break-even sales.

Use of PCG in Profit and Loss

The relationship between CP and SP is typically defined through a percentage relationship. As we have seen earlier, this percentage value is called the percentage markup. (And is also equal to the percentage profit if there is no discount). Consider the following situation suppose the SP is 25% greater than the CP. This relationship can be seen in the following

CP 25% increase SP

In such a case the reverse relationship will be obtained by the ABA application of PCG and will be seen as follows If the profit is 25% :

CP 25% increase SP 20% decrease CP

Suppose you know that by selling an item at 25%, profit the Sales price of a bottle of wine is Rs. 1600. With this information, you can easily calculate the cost price by reducing the sales price by 20%. Thus, the CP is

1600 20% decrease 1280

Profit Calculation on the Basis of Equating the Amount Spent and the Amount Earned

We have already seen that profit can only be calculated in the case of the number of items being bought and sold is equal. In such a case, we make the difference between the money got and the money given to get the calculation of the profit or the loss in the transaction. There is another possibility, however, of calculating the profit. This is done by equating the money got and the money spent. In such a case, the profit can be represented by the number of goods left. This is so because in terms of money the person going through the transaction has got back all the money that he has spent, but has ended up with some amount of goods left over after the transaction. These leftover items can then be viewed as a profit or gain for the individual consideration.

Hence, profit, when money is equated, is given by Goods left. Also, the cost, in this case, is represented by Goods sold

Percentage Profit = Goods left / Goods sold × 100.

Summary of Profit and Loss Formula

Given below are profit and loss formulas and tricks to derive the value of other terms from the basic fundamental formulas:

Solved Examples

Question 1:

I sell 16 sheep at a gain of 12.5% and 20 more at a certain gain percent. If 1 gain 25% on the whole, how much percent gain did I make on the latter number?

Solution

On the whole, I gain 25%

Therefore, I should get the cost price of 36×(125/100)=45 sheep.

But I sell the first lot at a gain of 12.5%

Hence by selling 16 sheep, I get the cost price of

16×112.5/100=18 sheep.

Therefore, I should get the cost price of 45-18=27 sheep by selling the second lot of 20.

Hence my gain there should be

7/20×100=35

Question 2:

Two oranges, three bananas, and four apples cost Rs. 15. Three oranges, two bananas, and one apple cost Rs. 10. I bought 3 oranges, 3 bananas, and 3 apples. How much did I pay?

Solution

It is given that

2O + 3B + 4A = 15 …..(1)

3O + 2B + A = 10…….(2)

The answer to this question seems to cannot be determined as we are given three variables but we can form two equations only. But the question is not asking about the individual price of 3 oranges, 3 bananas, and 3 apples but it asks for the cost of 3O + 3B + 3A. For that, if we add the two equations, we get

5O+5B+5A=25

O+B+A=5

Therefore 3O +3B+3A = 3×5 = 15

Question 3:

A dealer offers a cash discount of 20% and still makes a profit of 20% when he further allows 16 articles to a dozen to a particularly sticky bargainer. How much per cent above the cost price were his wares listed?

Solution

Let the CP of the article be Rs. x, since he earns a profit of 20%, hence SP = 1.2x.

It is given that he is selling 16 articles to a dozen, so he a incurs loss by

selling 16 articles at the cost of 12 articles [loss = {(16-12)/16} x 100 = 25%]

∴ His selling price = SP × 0.75

Now SP × 0.75 = 1.2 x⇒ SP = (1.2/0.75)x = 1.6x.

This SP arrived after giving a discount of 20% on MP.

Hence, MP = (1.6/0.8)x = 2x

It means that the article has been marked 100% above the cost price.